Ibiza Property Transfer Tax (ITP) Explained: What You'll Actually Pay

You've found your dream property in Ibiza. The asking price is €3 million. Your lawyer mentions the ITP, and you assume it's a straightforward percentage. Then you see the calculation, and the number doesn't match what you expected.

Here's what catches most buyers off guard: Ibiza's Property Transfer Tax isn't a flat rate. It's progressive, meaning different portions of your purchase price are taxed at different rates. Understanding exactly how this works, and what you'll actually pay, is essential before you make an offer.

What you need to know

ITP (Property Transfer Tax) only applies to resale properties, not new builds. New construction is subject to VAT instead.

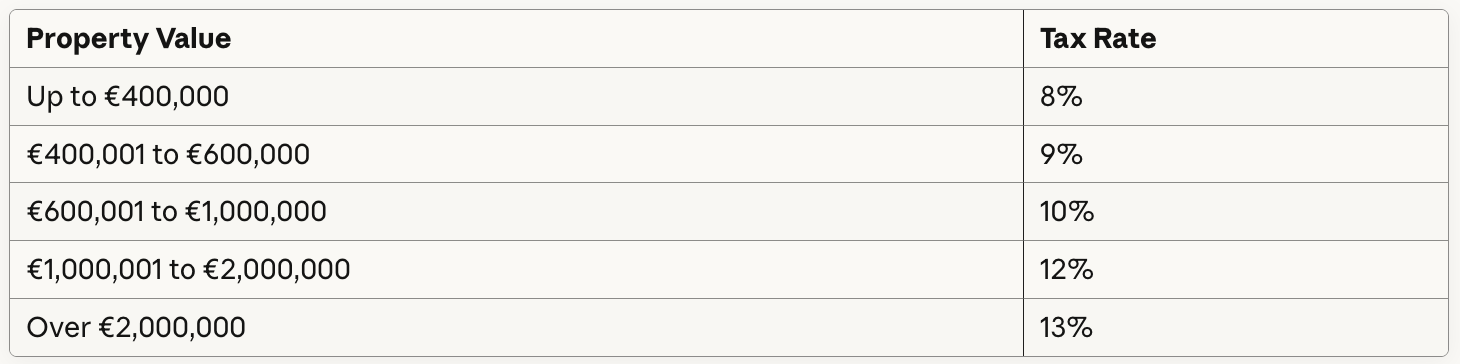

The tax is progressive, ranging from 8% to 13% depending on the property value. Each portion of the price is taxed at its corresponding rate.

You pay ITP at the notary signing and must file within 30 working days. Budget for this as part of your completion costs.

The progressive structure means crossing certain thresholds significantly impacts your total tax bill. A €2.1M property costs notably more in tax than a €1.9M property.

What Is ITP and When Does It Apply?

ITP stands for Impuesto sobre Transmisiones Patrimoniales, Spain's Property Transfer Tax. In the Balearic Islands, this tax applies when you purchase an existing property from a private seller or a company that isn't acting as a developer.

When you pay ITP:

- Buying a resale property from a private individual

- Buying a resale property from a company (when it's a second or subsequent sale)

- Purchasing shares in a Spanish company (SL) that owns real estate (anti-avoidance rules typically apply, see section below)

When you DON'T pay ITP:

- Buying a brand new property from a developer (you pay 10% VAT + 1.5-2% Stamp Duty instead)

- Buying land from a developer for the first time (you pay 21% VAT + Stamp Duty)

- Inheriting property (different inheritance tax applies)

The distinction matters because it fundamentally changes your purchase cost structure. This guide focuses exclusively on ITP for resale property purchases.

The Progressive Tax Structure: How It Actually Works

The Balearic Islands use a five-tier progressive tax system. Here's the breakdown:

What "progressive" actually means:

You don't simply multiply your entire purchase price by one percentage. Instead, each portion of the price is taxed at its corresponding rate.

Think of it like income tax brackets. The first €400,000 is always taxed at 8%. The next €200,000 (from €400,001 to €600,000) is taxed at 9%. And so on.

This structure means two things:

- Lower-priced properties have a lower effective tax rate (the average rate across all portions)

- Crossing a threshold doesn't suddenly make the entire purchase more expensive, just the portion above that threshold

Let's look at real examples to see how this plays out.

Real-World Examples: What You'll Actually Pay

Example 1: €350,000 Property

For a property below the first threshold, the calculation is straightforward.

Purchase price: €350,000

ITP calculation:

- €350,000 at 8% = €28,000

Total ITP: €28,000

Effective tax rate: 8%

This is the simplest scenario. Your entire purchase price falls within the first bracket, so you pay a flat 8%.

Example 2: €800,000 Property

Now we cross into multiple brackets.

Purchase price: €800,000

ITP calculation:

- First €400,000 at 8% = €32,000

- Next €200,000 at 9% = €18,000

- Remaining €200,000 at 10% = €20,000

Total ITP: €70,000

Effective tax rate: 8.75%

You're now using three tax brackets, but your effective rate is still well below the highest rate you're paying (10%).

Example 3: €3,000,000 Property

Purchase price: €3,000,000

ITP calculation:

- First €400,000 at 8% = €32,000

- Next €200,000 at 9% = €18,000

- Next €400,000 at 10% = €40,000

- Next €1,000,000 at 12% = €120,000

- Remaining €1,000,000 at 13% = €130,000

Total ITP: €340,000

Effective tax rate: 11.33%

Even at €3 million, your effective tax rate is below the top bracket rate of 13% because the lower brackets reduce your overall percentage.

Example 4: €8,000,000 Property

Purchase price: €8,000,000

ITP calculation:

- First €400,000 at 8% = €32,000

- Next €200,000 at 9% = €18,000

- Next €400,000 at 10% = €40,000

- Next €1,000,000 at 12% = €120,000

- Remaining €6,000,000 at 13% = €780,000

Total ITP: €990,000

Effective tax rate: 12.375%

At this high price point, most of your purchase price is taxed at the top rate, so your effective rate approaches (but doesn't quite reach) 13%.

The Threshold Effect: Why €100,000 Can Matter

One of the most important strategic considerations is understanding how crossing a threshold impacts your total cost.

Scenario A: €1,950,000 property

ITP calculation:

- First €400,000 at 8% = €32,000

- Next €200,000 at 9% = €18,000

- Next €400,000 at 10% = €40,000

- Remaining €950,000 at 12% = €114,000

Total ITP: €204,000

Scenario B: €2,050,000 property

ITP calculation:

- First €400,000 at 8% = €32,000

- Next €200,000 at 9% = €18,000

- Next €400,000 at 10% = €40,000

- Next €1,000,000 at 12% = €120,000

- Remaining €50,000 at 13% = €6,500

Total ITP: €216,500

The comparison:

The property in Scenario B costs €100,000 more in purchase price, but only €12,500 more in ITP. That's because only the €50,000 above the €2M threshold is taxed at the higher 13% rate.

This matters for negotiation. If you're looking at properties right around a threshold, understanding the actual tax impact helps you evaluate offers more accurately.

When and How You Pay ITP

Timeline:

ITP is paid when you sign the final deed (Escritura de Compraventa) at the notary. However, the formal filing and payment must be completed within 30 working days from the day after the notarized sale.

This means you need to have the full ITP amount ready for your notary appointment, along with the remaining purchase price balance.

How it's paid:

Your lawyer coordinates the payment and filing process. The ITP must be:

- Self-assessed by the buyer

- Filed using Modelo 600 (the regional tax form)

- Paid to the Agència Tributària de les Illes Balears (ATIB)

- Submitted within 30 working days of the sale

The process:

- Your lawyer calculates the exact ITP based on the declared purchase price (or the official reference value, whichever is higher)

- You transfer the ITP amount (along with other completion funds) to your lawyer's client account

- Your lawyer files Modelo 600 and pays the tax authority on your behalf

- You receive official tax payment documentation

- The notary completes the sale and registration

Important: Payment can be made online or at authorized banks. The 30-day deadline is strict. Missing it results in penalties and interest charges.

Buying Through a Spanish Company (SL) vs. Privately

A common question from international buyers: does purchasing through a Spanish company (Sociedad Limitada, or SL) affect ITP?

The short answer: You'll pay ITP either way.

Scenario A: Your SL buys the property directly

If your Spanish company purchases a resale property, ITP applies at the same 8-13% progressive rates. The company is simply the buyer instead of you personally, but the transfer tax obligation is identical. There's no ITP exemption for corporate buyers of residential property.

Scenario B: You buy shares in an existing SL that owns the property

You might think buying the company shares (rather than the property itself) could avoid ITP, since share transfers are generally tax-exempt. However, Spanish law has anti-avoidance rules specifically designed to prevent this.

When share purchases trigger ITP:

If you acquire more than 50% of shares in a company where:

- More than 50% of the company's assets are Spanish real estate, AND

- That real estate is not used in an active business

...then the tax authorities treat the share transfer as a property sale, making it subject to ITP on the real estate's market value.

In practice: Buying 100% of a Spanish property-holding SL (a common structure for Ibiza villas) will be liable for ITP just as a direct purchase would be.

Possible exception: If the company operates an active rental business or other economic activity (not just passively holding property), the share transfer might remain exempt. This is complex and fact-specific.

What to ask your lawyer:

- Is the SL's property used in an active economic activity?

- What percentage of the company's assets is real estate?

- Has the company been filing tax returns consistent with an active business?

- What documentation exists to support the business activity claim?

Your lawyer can assess whether the share purchase route genuinely avoids ITP in your specific case, or whether you'll face the same tax obligation as a direct purchase.

Bottom line: Don't assume buying through or from an SL saves ITP. In most typical scenarios (a villa owned by a holding company), you'll pay the same transfer tax either way.

Common Questions About ITP

Can I reduce my ITP by declaring a lower purchase price?

No. This is illegal and carries serious penalties. The declared price must match the actual price paid.

Additionally, the tax base for ITP is the higher of:

- The declared purchase price, OR

- The official reference value (valor de referencia catastral)

Spanish tax authorities use this official reference value as a benchmark market value. If they believe your declared price is suspiciously low compared to the reference value, they can challenge the declaration and assess ITP on the higher amount.

Penalties for under-declaration include fines, back taxes calculated on the correct value, interest charges, and potential criminal charges for tax fraud.

Does my nationality affect ITP rates?

No. Spain does not impose higher property transfer tax rates on foreign buyers. Whether you're an EU citizen, non-EU citizen, resident, or non-resident, the ITP rates are identical.

Both EU and non-EU buyers pay the same 8-13% progressive ITP rates, must obtain a Spanish NIE (foreign identification number), and follow the same filing and payment procedures.

The only practical difference: non-resident buyers typically don't qualify for the reduced ITP rates available for primary residences (see below), as those require you to make the property your habitual residence and meet specific residency criteria.

Are there any ITP reductions or exemptions available?

Yes, but most international buyers won't qualify. The Balearic Islands offer reduced ITP rates (ranging from 0% to 4%) for specific cases, such as first-time buyers purchasing a primary residence under certain price thresholds, young buyers, large families, or those with qualifying disabilities.

Important limitations: These reductions only apply if the property will be your primary residence (vivienda habitual), you don't own other residential property, and you maintain it as your main home for a minimum period (typically 3 years).

Most foreign buyers purchasing in Ibiza won't qualify because the property is typically a second home or investment, not a primary residence, and non-residents don't meet the habitual residence requirements.

If you're relocating to Ibiza permanently and will become a Spanish tax resident, consult your lawyer about potential eligibility. Otherwise, budget for the standard progressive rates.

Is ITP tax-deductible?

For Spanish tax residents, ITP generally cannot be deducted from income tax. However, if you're renting the property, the ITP becomes part of your property's cost basis, which can impact capital gains calculations when you eventually sell.

For wealth tax purposes, the property value (including ITP paid) can be relevant to your overall asset calculation.

Consult with a tax advisor familiar with your specific residency and investment situation.

Can I pay ITP in installments?

No. ITP must be paid in full within 30 working days of the notary signing. There are no installment options. This is why it's essential to have your full financing arranged before completion, including the amount needed for taxes.

What happens if I don't pay ITP on time?

Missing the 30-day filing deadline results in penalties and interest charges. The notary cannot complete your registration without proof of ITP payment, which means you will not legally own the property until the tax is paid.

This is another reason why working with an experienced lawyer who coordinates all payments and deadlines is essential.

Strategic Considerations

Understanding ITP helps you make smarter decisions during your property search and negotiations:

1. Budget accurately from day one

When you tell your real estate advisor your budget, clarify whether that's your total available funds or just the property price. A €3 million budget including costs means you're actually looking at properties around €2.65 million.

2. Factor ITP into negotiations

If you're negotiating on a property near a threshold, knowing the exact tax impact helps you evaluate what's actually achievable. A seller reducing price from €2.05M to €1.95M saves you €12,500 in ITP beyond the €100,000 price reduction.

3. Compare resale vs. new build fairly

When evaluating a €3M resale property (€340,000 ITP) against a €3M new build (€360,000 in VAT + AJD), the resale actually costs €20,000 less in taxes. But new builds offer other advantages like modern construction, energy efficiency, and customization. Compare the full picture, not just the headline price.

4. Plan your completion funding

Know exactly when you need each amount. The 10% deposit comes at the Contrato de Arras signing (Week 3-4), but the ITP and remaining 90% come at notary completion (Week 8-12). Your lawyer must then file and pay the ITP within 30 working days. If you're arranging financing, ensure it's structured to release funds on the right timeline.

In Summary

Ibiza's Property Transfer Tax is progressive, not flat. For resale properties, you'll pay rates ranging from 8% on the first €400,000 to 13% on amounts over €2 million. Your effective tax rate will always be lower than the highest bracket you reach because earlier portions are taxed at lower rates.

For a €1.5 million property, expect to pay €150,000 in ITP (10% effective rate). For a €3 million property, expect €340,000 (11.33% effective rate). For an €8 million property, expect €990,000 (12.375% effective rate).

This tax is paid at the notary signing and must be filed within 30 working days using Modelo 600. Budget for total acquisition costs of 10-14% above the purchase price when planning your finances.

The progressive structure means crossing thresholds matters, but not as dramatically as you might think. Understanding the real math helps you negotiate effectively and budget accurately.

Whether you buy privately or through a Spanish company, you'll pay ITP. Whether you're an EU or non-EU citizen, the rates are the same. Most international buyers won't qualify for the special reductions available for primary residences.

Ready to understand your complete purchase costs for a specific property? Our team can provide detailed cost breakdowns tailored to your budget and requirements. Contact us to discuss your Ibiza property search.

Please note: This guide provides general information about ITP in the Balearic Islands as of 2024. Tax rates and regulations can change. We strongly recommend consulting with a qualified tax advisor and lawyer familiar with Spanish and Balearic tax law for advice specific to your situation.

.jpg)